Paying Off Debt – The Definitive Guide

If you are tired of being in debt and need a lifeline– then this article is for you. In fact, this whole site is for you. Rest assured, I have no intention of making you feel bad for the situation that you are in. I can’t do that, because I was in the exact same place just two short years ago. It was then that my wife and I came together, made a plan, and worked our way out from over $20,000 in credit card debt. We didn’t consolidate our bills, we didn’t use a debt relief service, and we didn’t borrow any money from friends or family. We paid off our debt the hard way and did it in just fourteen months using the process that I will describe below.

We came out of the whole experience with a new understanding of the way that money works, and a new appreciation for everything that we have. You can read our debt story here and here, but this guide isn’t about us- it’s about YOU. It’s about how you can take the first few steps to begin the process that will create the financial future that you deserve.

You may think it is overly ambitious to attempt to capture a debt payoff strategy in a single post, when there are multi-week courses and an entire genre of books dedicated to the topic. However, I’d like you to think about this post a little bit different. By reading through the article below, you will get a basic understanding of how my wife and I paid off our consumer debt. If you are ready for it, this same strategy can work for you.

Level Setting About Paying Off Debt

The very first thing you will need to accept is that things are going to have to change. We all know that change isn’t easy, but your current path is simply not sustainable. You just aren’t making enough money to live the way that you do. If you can’t accept that, then you have zero chance of fixing this situation. You must also be willing to alter your understanding of what money is and what it does for you. We are taught from a very young age that money is the key to happiness, but decades of research has definitively shown us that it doesn’t really work this way. You must learn to find other ways to deal with boredom, stress, and jealousy– emotions that often cause people to spend and then spend some more. Let’s get started.

Budgets

Yes, budgets are indeed a bummer. So much so, that the very thought of sitting down and creating a budget is painful enough to keep many people from even getting started down a better financial path. Nobody wants to spend a few hours each week tracking every single penny, but desperate times call for desperate measures.

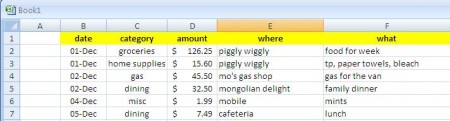

Around here, we like to call it “Budgeting in the Weeds” and I am going to ask you to commit to spending JUST ONE month doing exactly that. During this month, write down ALL of your outbound and inbound money. Every single penny. There are programs (like You Need a Budget) available that make tracking expenses fairly easy, and they let you try their software for free for 34 days (which should be all that you need). However. if you don’t want to learn any new software, a simple spreadsheet, as shown below, will do just fine.

It’s important when tracking expenses that you resist the urge to “cheat” and omit some expenses. The breakfast that you grab on the way into work must be included. The weekly manicures have to count. Again, nobody is judging you here! You are just doing research to figure out how bad the situation really is. To make tracking easier, I would recommend that you stop using cash entirely and do all of your purchasing with your debit card. Many of the financial gurus of the world would recommend that you switch to using entirely cash, but having a digital record of your expenses helps to make sure that all of your purchases are out in the open.

This is also the time to start trying to somewhat keep spending under control. You don’t need to go extreme cheapskate and limit yourself to one square of toilet paper, but you shouldn’t be buying yourself a new wardrobe or purchasing any concert tickets during this time. That type of discretionary spending might necessitate reaching for the credit cards, and that was the old you. Trust that there will be a day when you can once again buy a new outfit without worry, or take your family on a trip. It’s just not today.

Speaking of which, if you haven’t already, go ahead and cut up your credit cards. You aren’t going to need them anymore. If you can’t afford it without using your credit cards, it will

have to wait. And when it comes to making payments against those cards, just pay the minimum for now, even if you have the ability to pay more. We will get to the debt slaying soon enough, but first we need to make

sure that we can ride with training wheels without tipping over.

A Quick Analysis

If you find that you are still in the red, even with paying the minimum on your credit cards– then you are going to need to act quickly. You will need to find a way to both cut costs *and* earn some additional income as soon as possible. We’ll get into some ideas for both of these shortly, but please understand that the consequences for not paying your bills can be devastating.

If this is your situation, then the first thing you should do is to call your creditors to explain the situation. Be honest and tell them that you are in over your head, and ask if they have a hardship plan where you can make reduced payments for a period of time. Tell them that you are taking on additional work, and are currently undertaking an austerity plan that will allow for you to resume making normal payments in a month or two.

If your budget shows a small amount of breathing room, then you don’t get off easy either, friends. When you are in debt, any “breathing room” you feel is only imaginary. Those banks own your butt, and until you get rid of that debt– you don’t get to decide where your money goes. Your goal from here on out is going to be to take that breathing room and expand it.

Every bit of extra money that you have, will be used to pay off debt. Yes, this journey will be long and boring, but it is absolutely essential. There is no reason to feel sorry for yourself as you undertake this journey, because this path is the only way out. Many others have gone before you, and their lives have been changed forever as a result of it.

The Emergency Fund

Back when my wife and I were having our troubles with debt, I had never even heard of the concept of an emergency fund. It even seemed a bit anti-logical to begin our debt payoff plan by dropping $1000 into a savings account instead of jumping right into attacking our credit cards, but that is exactly what you must do. Personal finance bloggers rightfully love to talk about emergency funds, because they are all about changing your mindset.

To put it simply, there WILL be setbacks during this great debt payoff adventure that you are beginning. Your credit cards are gone, and they are no longer an option for you. Instead, your emergency fund will be there when you need it. Emergencies are just a part of life, and these unexpected expenses are actually the #1 contributor to credit card debt with most families. What you need to create is a buffer so that when these emergencies do happen, you can pay for them without adding to your overall debt.

If you have any money leftover after your first frugal month budgeting in the weeds, I want you to put it into an emergency fund. If you don’t have a savings account, you can open a Capital One 360 account right now and get a $25 bonus to help get started. For the next few months, continue to pay the minimum on all of your credit cards and instead funnel any and all extra cash into this emergency fund. Keep doing this until you have $1000 saved up. Live frugally, and start to keep an eye out for opportunities to earn extra income, because the quicker that you hit that $1000 mark, the sooner you can get started paying off debt.

Snowballs

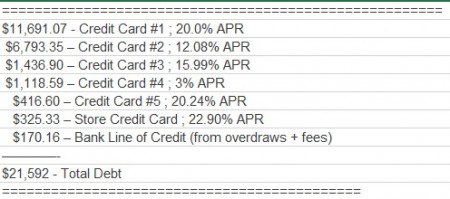

Now that we understand what your baseline budget looks like and have built up an emergency fund, we need a strategy for taking down your debt. If you are like many people, chances are good that your debt is spread across a variety of credit cards. To start, we are going to need to do some research. Again, all that you should need is a simple spreadsheet. List your debts one by one, and for each one– list the amount that you owe, and the interest rate that you are currently paying. This information should be available on the lender’s website. If you can’t find it, don’t hesitate to call the number on the back of your card and ask them. If you look back at the early days of this blog when we were first formulating our plan of attack, this is exactly what we did. When you are done, the spreadsheet should look something like this:

Among the experts, there are some varying opinions when it comes to the order that you should pay off your credit cards. Some would tell you to use some simple math and pay off the highest interest credit cards first, while paying the minimum on the rest. Others would instead suggest paying off the cards with the smallest balances first, just to give yourself some “quick wins” for positive reinforcement.

The most important thing here is that you STOP USING YOUR CARDS. This is where most people get into trouble. It doesn’t matter which approach you take if you are still piling dirt on the top of the mountain. I can see the value in both approaches, and for our own debt payoff we went with a bit of a hybrid of the two options. Any debt that was at 0% interest (more on this in the next section) went to the back of the line, but for the most part– we attempted to zero out the lower balances first (thus reducing the number of overall payments that we had to worry about). For our highest interest debt, we tried to utilize balance transfer math to help lower the overall amount of interest that was being paid.

The Balance Transfer Game

It’s natural to have a little bit of fear of credit cards when they have gotten you in trouble. That said, we did utilize credit cards and their promotional zero-interest offers to help us get out of debt. Our plan was to transfer a high-interest balance over to one of these cards in full (we only did it if we could transfer the entire balance), and then we would immediately cut up the new card to make sure that we didn’t use it.

For example, I remember transferring an $8000 balance to this card during our repayment phase. This particular offer was (and still is) a zero percent interest on balance transfers for 12 months, which was available at the cost of a 3% balance transfer fee. This fee sounds a bit scary since your total debt will actually go up, but the math ends up working to your advantage. With a balance of $8000, the transfer fees were $240 (3%), which was added to the balance immediately.

From there, we started paying down this debt with everything that we had and ended up paying off the balance completely within the 12 month period, thus paying 0% interest on that balance from there on out. If we had continued to pay the 20% interest on that amount the entire time, it would have cost us well over $1000 in interest costs alone (even with the decreasing balance)! You can check out the numbers for your own situation using this tool: Balance Transfer Calculator.

Making More Money

You can play all the games you want with building snowballs and moving debt around, but at some point you are going to have to get into the nuts and bolts of making more money than you spend. Yes, you will likely need

to find places in your budget where you can cut spending, and we’ll talk about that in a minute. But the easiest and best way to pay off debt quickly is to find ways to make more money,

and to apply that extra money directly against your debt.

You think that frugal living is boring and frustrating? Well, the more money that you make, the quicker you can move into the next phase of your life. This means that it is time to get creative. If you have a job, then it’s time to start building your value so that you can be comfortable asking your boss for a raise. At the same time, start spending your free-time looking for additional ways to make income.

Perhaps you could start looking on Craigslist for people that need assistance with something. Maybe you could look into starting a blog to make some extra money or perhaps creating >a niche site. There are dozens of ideas for generating extra income that have been shared on this site, so please feel free to explore our archives.

I would also recommend keeping an eye on See Debt Run in the months and weeks to come, as we will soon be releasing some new resources that will help you develop strategies for finding extra cash. Also, we should probably take a minute to talk about material possessions. If you have a bunch of “collectibles” lying around your house at the same time that you are carrying debt, then you may have to answer a difficult question: What do you value more? These things, or your family’s freedom? If you don’t have a use for something in your day-to-day life, and selling it can bring some extra income that you can use against your debt, then you shouldn’t be afraid to sell it. You can always buy another one when you can truly afford it, of course.

Cutting Costs

Earlier in this article, I suggested that you needed to cut back on discretionary spending while getting a “baseline” on your budget. The truth is, you really should continue living frugally until you have finished paying off your debt. I know this might sound depressing, but you have to reassure yourself that this austerity plan is only temporary. I don’t recommend going completely cold turkey and removing all joy from your life, as this can rapidly lead to frustration and giving up on your debt repayment agenda altogether.

I am a strong proponent of leaving behind a little bit of “fun money” even when you are in debt reduction mode. You can still buy yourself a coffee in the morning, but perhaps only do it once a week instead of every day. You can still go out to eat, but just try to do it a little less often and avoid ordering drinks when you do go out. You don’t have to avoid replacing broken appliances or cancel Christmas or anything like that– but you definitely should start to consider the cost of things in the decisions that you make.

One of the most difficult parts of the debt reduction journey for my wife and me was when we had to tell our kids that we wouldn’t be going on any vacations until we had paid off our debt. We invited them into the journey, and tried to help educate them on how debt happens, and how it can be avoided. To avoid getting frustrated when saving money, it can be good to try and embrace frugality as a new hobby of sorts. Take pride when you figure out a way to do something cheaper; you now have a leg up on the rest of society! Remember, the more money you are able to knock off your monthly budget, the more that you will have to allocate towards debt reduction.

There are hundreds of other money-saving ideas that have been discussed on this website and many others. Some of these measures are more difficult than others and you certainly don’t need to do them all. Here are a few to get your started:

- Start meal planning and couponing to see if you can knock a few hundred dollars off your food budget.

- Join a carpool to work or try to work from home once or twice each week to save on fuel costs.

- Keep the thermostat a few degrees colder in the winter, and a few degree warmer in the summer.

- Cancel your cable or at the very least stop paying for the movie channels that you never watch.

Living a Life Less Ordinary

After you’ve started down the debt-repayment path, there really isn’t any magic to it. You pretty much just rinse and repeat, month after month, until the debt is gone. Things do certainly start to accelerate as you start to zero out balances, because you can take the minimum payment that you were paying, and toss it against the next balance on your list. As time passes, you will also likely get better at both saving money and finding ways to make extra income. The biggest challenge of all is just getting started. If you are in debt and found your way to this article, then you already have the curiosity. My hope is that you can use our story as motivation, and use this article as a guide to help you get started. Good luck and God bless!

Great article. I can testify that paying off your debt has incredible emotional (and of course monetary) benefits. It’s worth the struggle of changing habits and mindset. Also, I had to practice budgeting several times before I got the hang of it and effectively changed my habits. Getting rid of my credit card was huge. And after a while it becomes second nature and you don’t have to track every penny because you have a good idea of how much you are spending.

No doubt, Edson. It is a challenge, but the rewards are immense. Living a life with financial freedom just changes your whole outlook.

I just discovered your blog yesterday and subscribed. Now you publish an epic post like this and I’m starting to realize what a good decision I made 😉

There really are so many golden nuggets here and having paid off a lot of debt myself over the last couple of years all of what you say rings true with my experiences. I especially loved this…

“You can play all the games you want with building snowballs and moving debt around, but at some point you are going to have to get into the nuts and bolts of making more money than you spend.”

Genius 🙂

Thanks for the kind words, Richard. I tried to sprinkle in a little bit of tough love throughout the article, as sometimes people need to hear it.

Budgets are a bummer. They are a necessary evil though. I am still trying to figure them out even after all this time. Spending less than what you have is very important to me.

Yeah.. You have to jump in and budget if you want to truly get control over your finances.. There really is no other way.

I love this. It’s like two years of blogging, all in one post!

Nice article Jefferson. Playing the balance transfer game was key to me paying off my debt. I played that game for four years and feel that I won in the end. I reduced my interest rates and saved quite a bit over the journey.

I think many people are afraid to do this but the numbers don’t lie. Thanks for commenting, Grayson.

It’s always encouraging to hear from some who has been there and know that the advice REALLY works. Thanks for continuing to inspire.

Thank you Stefanie.. My biggest hope in running this site is that it can motivate others who were/are in a similar situation.

This is a great article! I am in the process of working to pay off debt (hoping to have it paid off by the end of this year!). In fact, just went back to my budget today to see where I could work in a few purchases that we are planning along the way. Great tips!

We paid off our debt the hard way <— I'm not sure that there's an "easy" way to pay off debt other than getting a huge gift of money or winning the lottery. Utilizing a debt relief program (if your finances are so far gone that you need a hand in getting yourself out of the ditch), or utilizing a debt consolidation loan to get a lower interest rate (and lower payment) are useful tools to be used in conjunction with all the great information you have here in your post. Learning how to track your expenses, budget your money, and use self control to live within the confines of your income are all things that someone getting out of debt need to learn how to do better (or in our case, learn how to do period). Congratulations on your success in getting things back on the rails in such a short period of time, Jefferson!

Good point, Travis.. I may have glossed over that fact a bit.. After 3000 words, my fingers were getting tired 🙂

For many people, a debt relief program can be just the lifeline that they needed. There is absolutely nothing wrong with using one, and there is no doubt that they help provide lifelines for many people who are swinging in the dark, paralyzed by their situation.

Awesome post, Jefferson. Love the thoroughness and honesty here, and I can attest as someone who took the above steps and started a debt-payoff journey just over a year ago that, in spite of the work, the boredom, etc., it is totally and completely worth it.

Great post! You definitely covered all of the bases. Budgeting and tracking our spending were probably the most helpful things we did when we started out.

Thanks Holly.. Tracking your spending is definitely more than most people do!

Wow! Love the post Jefferson. I’ve loved watching you and Michelle crush it here. Cutting lifestyle and creative ways to save in multiple areas of your budget is such a powerful tool. Can’t wait to see how many people get motivated and out of debt after reading this.

Thanks for the kind words, Nick. This website did wonders for keeping us accountable back when we were “crushing it”.. I like to think that we still are, just in a different way 😉

I really enjoyed this post!! Thanks for sharing. I’m working on my debt snowball. Thankfully, I am no longer in credit card debt – but I am working to pay off my student loan (on a 0% card, so I guess it’s “considered” CC debt), car loan and mortgage.

So happy to hear that Maria!.. I know that you can do it!!

You’re right, Jefferson. It’s pretty much rinse and repeat, month after month… after month. That’s why it’s so hard to do. Because sacrifice over the long term isn’t fun at all.

Thanks for sharing your story and helping us get (and keep) or financial act together!

Talk about a comprehensive guide! I’ve never had debt, so I always feel a bit awkward commenting on or heaven forbid criticizing how others dig their way out. In the end, it’s just awesome to make it a priority and get yourself back in black! I’ll certainly be sharing this with friends/followers who have questions about debt repayment strategies.

No worries.. Good for you for never having to do deal with the frustration that is trying to pay off debt. There are lots of reasons why people end up in debt, but the important thing is being motivated to make your situation better!

Great comprehensive article, Jefferson! Debt repayment is definitely a journey but the payoff is huge! 🙂 When people start tracking their spending, it can be really eye-opening. There are so many little things we pay – like mints, soda, gum, lunch that we forget about them but they add up quickly. I also think a changed mindset is necessary too. To realize that the freedom you believe your credit offered offers is an illusion. Credit cards are not evil but can be easily abused. The real freedom is being able to make choices based on what you want without creating debt. I’m so glad your enjoying true freedom now and helping others find their way too.

I like this tip “it can be good to try and embrace frugality as a new hobby of sorts”. I have to admit this is something I didn’t embrace early enough. But now I see the benefits so much clearer. You’ve outlined a nice plan here.

Thanks Raquel. I liked that part too and hope that it resonates with people. You can choose to focus on destructive or productive patterns in your life, and they will have a great impact on whether or not you can meet your goals.

I like your point about tracking ALL of your expenses. I know I am guilty of using cash on occasion just so I don’t have to look at the expense later on my credit card bill! I pay cash so I can just forget about it.

I think one of the key things you’ve pointed out is our tendency to connect money to emotional problem solving. Whether we’re meeting emotional needs by buying things or coping with stress if money is connected to your emotions you’re going to have issues with it. Making some sort of healthy separation between your emotions, identity and money is a great first step in creating a helpful budget and being able to stick with it. This is a very elaborate outline, I appreciate the work that went into it.

I’ve done a lot of this, including making more, cutting costs, and using balance transfers to make my debt a bit more affordable. My biggest mistake was using my e-fund to pay off debt. It definitely came back to haunt me recently and I had to charge an emergency :(.

Yeah.. You need to make sure that your e-Fund stays available and ready. Emergencies will always happen, sometimes with the very worst timing possible.

I’ve been thinking of paying more on my debt this year and be able to be debt-free this year. I have listed down things and I hope plans will be pursued along the way.

Very well written article! It is very concise, but covers the main points required to get out of debt.

My wife and I have been there, done that with credit cards. We both brought debts into our marriage. She got herself into trouble and started down the path to recovery before we met. It took me a while longer to start working on my debt.

We found Dave Ramsey, and even though our progress was not perfectly “Gazelle Intense”, we did get rid of all debts. We are now a single income family by choice, which was impossible when we were in debt. Money is still tight, but God is good, and provides what we need.

We have gotten lazy about using our budget lately, and because I don’t want to end up in the same boat, I started back this month. The desire to start budgeting again is what led me to your site.

I just saw your post for the first time today and I’m in. If you can help me reduce my cr.card debt that will be fantastic. Only thing is, I may have to tweek it a bit as I live in Canada and some of what you may have to have helped you may not be available here. I’m able to pay above the minimum payments and have been, but according to my cr.card budgeter that I found online, it’s gonna take me 46yrs to pay it off. If I can do it in 2 years or 3, I’ll be ecstatic!! And, I’ll even post that I did it with your help as you will deserve the credit. Thank You so much!!

P.S. Can you tell me which surveys really do pay?? The only ones I’ve seen are like for maybe .75 and no payout till you’ve reached $5-$10.00

Only effective way for paying of all debts is to make more money.

Cutting costs is stupid and lefts you without joy in life.

If you are Over-spender then no system will help you to pay of your debts, because, if you earn more, you will spend more and you are at begging with bigger debts.